by Brad Hershbein

With ever-growing concern about rising student debt, American skill levels relative to other countries’, and the threat of automation for job growth, it would seem strange to remove benefits designed to make higher education less expensive for Americans. But that’s one set of provisions in the tax bill passed by the U.S. House of Representatives and being reconciled with the Senate version. The House-passed bill would:

- repeal the student loan interest deduction

- tax endowments of wealthy colleges (the Senate bill would do this, too)

- get rid of the Lifetime Learning Credit

- make newly taxable tuition waivers for employees of colleges and for graduate students serving as teaching or research assistants

- restrict employers’ reimbursements for employees’ educated expenses

The benefits slated to disappear are disproportionately ones that target education for older students, both graduate students and lifetime learners that need new skills to keep up with employers’ demands. Indeed, several commentators have sharply criticized the House bill for shortchanging graduate students, and the consequences for inequality among students of color. How could the bill specifically affect these students?

Graduate students

Among graduate students, 8 percent, or more than 290,000 people, received at least a partial tuition waiver in 2011–2012, the most recent year in which data are available. Two in five of these are PhD students, but more than half are Master’s students. About half of them work, not counting research or teaching assistantships, and one-third are students of color.

Excluding the value of their tuition waiver from their income, as in current law, students receiving a tuition waiver have an average adjusted gross income of a little over $33,000, although one quarter take in less than $9,000, and one quarter make over $42,000. The average tuition waiver is $8,700, but it’s closer to $13,000 for PhD students, who are concentrated at private research universities.

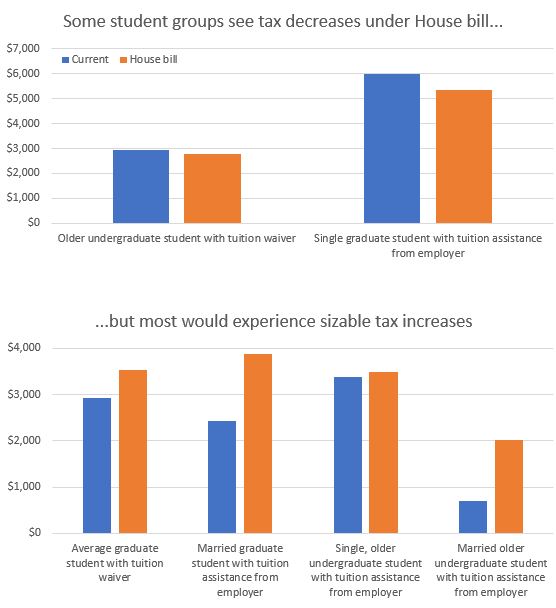

EFFECT: If this income were to become taxable, the average graduate student could see her taxes rise by more than $600, or 21 percent.[i] For a student making only $9,000 but getting an average-sized tuition waiver, taxes would rise from $0 to $660.

Older undergraduate students

Nearly 400,000 undergraduate students also receive tuition waivers, and one-third of them are over the age of 24. These older students have an average adjusted gross income of $33,000, basically the same as for the graduate students. Their average waiver is smaller, however, at $2,500.

EFFECT: Since these older students are financially independent (by definition), their tax bill would also change, but because of the smaller waiver, their taxes would actually fall slightly, by $128.[ii] Those with larger waivers, however, could see their taxes rise.

Working students getting tuition assistance from their jobs

Another major provision that tends to help older students is employer assistance with tuition. Currently, employers may pay for up to $5,250 per year toward tuition for their employees, without this money being taxable for the employee. This benefit is more common than tuition waivers among both graduate students (14.5 percent, or 530,000 students) and undergraduate students (5.7 percent, or 1.3 million students).

It can also be more valuable, with 43 percent of assisted graduate students and 20 percent of assisted undergrads receiving at least $5,250. Given the necessary relationship with an employer to be eligible, students receiving this benefit are more likely to work full-time, be older, and be married. They also have higher incomes, with average adjusted gross incomes of $51,400 for graduate students and $36,000 for independent undergraduates.

EFFECT: For a single graduate student getting at least $5,250 in assistance and with average income, taxes would fall from $5,989 to $5,334, about $655. For a married graduate student with the same employer assistance and income, taxes would increase by more than $1,400, from $2,443 to $3,870.[iii]

For a single independent undergraduate with at least $5,250 in assistance and with average income, taxes would increase slightly, from $3,374 to $3,486. For a married undergraduate student with the same employer assistance and income, taxes would increase by more than $1,300, from $710 to $2022, nearly tripling.[iv]

Conclusion

Although the House’s version of the tax bill may help a few older students, it is likely to substantially increase taxes for most older students, particularly if they are married or receive larger amounts of tuition assistance. It’s not clear to what extent these students, facing higher tax bills, would be less inclined to continue their schooling, or simply borrow more money and become more indebted. What is clear is that the bill is unlikely to promote the more-educated and more-skilled workforce that employers increasingly demand.

[i] The calculation assumes an adjusted gross income of $33,000 and a tuition waiver of $8,700 and a single person without dependents. Under current law, the standard deduction of $6,350 and personal exemption of $4,050 reduce taxable income to $22,600, $9,325 of which is taxed at 10% and $13,275 of which is taxed at 15%, for a tax bill of $2924. Under the House plan, adjusted gross income would rise to $41,700, and the standard deduction would rise to $12,200, but the personal exemption would be eliminated, so taxable income would be $29,500. The new tax rate would be 12 percent on this income for a tax bill of $3540.

[ii] Under the same assumptions, the initial tax bill is the same as for graduate students, since the income is (approximately) the same. Adjusted gross income would rise to only $35,500, and taxable income to only $23,300. At a tax rate of 12 percent, the tax bill would be $2796.

[iii] For a single graduate student filer and under current law, taxable income is $41,000 and the tax bill is $5989. Under the House plan, with the employer assistance taxable but with a different tax schedule, taxable income is $44,450, and the tax bill is $5334. For married joint filers with the same adjusted gross income, taxable income is $22,500 and taxes are $2443 under current law, but taxable income is $32,250 and taxes are $3870 under the House bill.

[iv] For a single undergraduate student filer and under current law, taxable income is $25,600 and the tax bill is $3374. Under the House plan, with the employer assistance taxable but with a different tax schedule, taxable income is $29,050, and the tax bill is $3486. For married joint filers with the same adjusted gross income, taxable income is $7100 and taxes are $710 under current law, but taxable income is $16,850 and taxes are $2022 under the House bill.

Experts